How to Buy Land and Subdivide It for Profit

How to Buy Land and Subdivide It for Profit Table of Contents Introduction Land Scams

While the process is simple in concept, understanding the mechanics of each component ensures you negotiate confidently and avoid costly mistakes. Here’s a deeper dive:

Unlike standardized bank mortgages, owner financing involves a direct agreement between you and the seller, allowing for flexible terms customized to both parties’ needs:

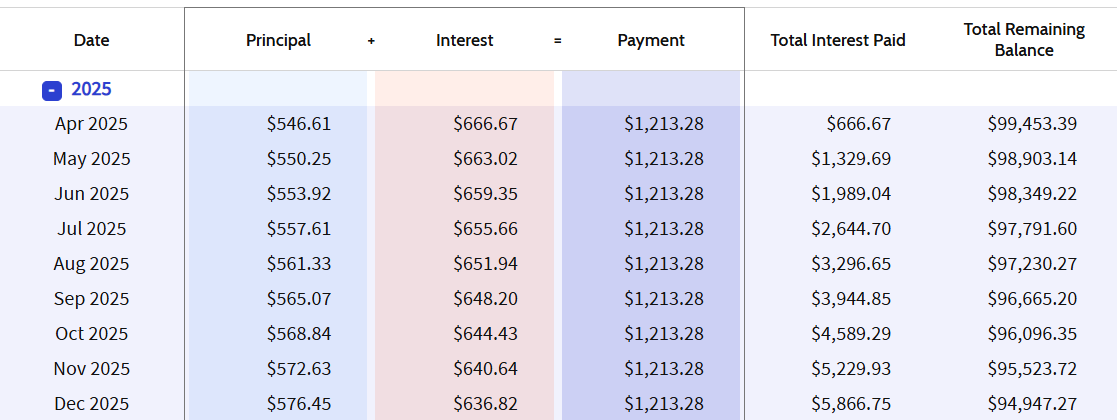

Tip: Use a loan amortization calculator to model payments. For example, a $100k loan at 8% interest over 10 years results in monthly payments of approximately $1,213.

Bypassing banks isn’t just about speed—it’s about control:

Example: A self-employed buyer with irregular income secures land through an owner finance arrangement with the seller.

Your payment isn’t “renting to own.” You assume ownership from the land on day one and build equity as the loan principal is paid down:

Amortization Example: To better illustrate how monthly payments break down between principal and interest, let’s look at an example of a $100,000 loan with an 8% annual interest rate over a 10-year term. The monthly payment for this scenario is approximately $1,213.28.

Here’s a breakdown for the first (2025) and last (2035) years:

**See full amortization schedule here.

The legal structure used to transfer ownership in owner financing is critical. While variations exist, it’s important to understand the most common and recommended instruments:

Red Flags to Avoid:

Owner financing isn’t “one deal fits all”—it’s a custom financial instrument. The more you understand these levers (interest rates, amortization, title transfer), the better you’ll negotiate.

Now for the exciting part: turning the power of owner financing into your 0 down land acquisition strategy.

Before making offers, you need to know exactly what you can afford.

The key to a $0 down deal lies in identifying sellers who are highly motivated to offer financing.

Target Specific Seller Profiles:

This step guides you through the initial conversation with the seller, focusing on understanding their price expectations and subtly introducing the concept of owner financing as a flexible alternative to a large down payment.

Example: Let’s assume you’ve found a piece of land listed for $75,000 and you’re calling the seller to discuss your offer.

A. Building Rapport and Understanding Seller Motivation

You: “Hello, my name is [Your Name], and I’m calling about the land you have listed at [Property Address/Location].”

Seller: “Oh, hello [Your Name]. Yes, it’s still available.”

You: “Great. It looks like a wonderful piece of property. Could you tell me a bit more about why you’ve decided to sell?”

Seller: “Well, I inherited it a few years ago, and honestly, I don’t have any immediate plans for it. The taxes and upkeep are just becoming a bit of a hassle.”

You: “I understand. And what is your current asking price for the land?”

Seller: “$75,000.”

You’ve established contact, shown interest, and subtly uncovered a potential motivation (avoiding hassle and costs). You’ve also confirmed the asking price.

B. Shifting the Focus to Terms – Introducing Owner Financing

You: “Thank you for that. The property definitely sounds interesting. As I explore my financing options, I wanted to ask if you’ve ever considered selling the land on terms?”

Seller: “Terms? What do you mean?.”

You: “It’s essentially where you, as the seller, are the bank. Sometimes, sellers find it beneficial because it can attract a wider range of buyers and potentially lead to a quicker sale at a higher price. It can also provide a consistent monthly income stream for you.”

Seller: “Why would I ever do that? I’d rather just get all the money at closing and be done with it..”

You: “That’s exactly why I brought it up. Most sellers want to sell for the highest price possible, even if it means that some of the money gets paid over time. I’d be happy to make you a cash offer, but if I paid you in all-cash I’d have to be at $40,000 instead of the $75,000 you’re asking”

You’ve introduced the concept of owner financing and highlighted potential benefits for the seller, directly linking it to her stated motivation (income). You’ve also trained the seller to understand the see-saw relationship between price and terms. Now let’s say you’ve gotten the seller’s attention and they’re open to learning more.

C. Exploring the Price-Terms Relationship

You: “That’s good to know. If you were to consider owner financing, what would be your ideal monthly payment from a buyer?”

Seller: “Well, I haven’t really thought about a specific number… maybe something around $500 to $600 a month would be helpful.”

You’ve successfully shifted the focus to the seller’s’s desired monthly income, a crucial piece of information for structuring your offer.

D. Exploring the Down Payment and Price/Terms Relationship

You: “Okay, that’s helpful – a monthly payment in the range of $500 to $600 is doable. However, since I’d be paying you your price and giving you the income you’re looking for, I wouldn’t normally offer a down payment, but I’m open to discussing it if that’s something that was important to you.”

Seller: “I’m a little hesitant about no down payment… I’d want to feel secure.”

You: “Absolutely, security is key for both of us. It’s also important to consider that with owner financing, the land itself serves as collateral. If I ever defaulted on payments that would be the best case scenario for you because it would mean that you’d keep all the payments you’ve received to date and you’d get the land back too..”

You’ve addressed the seller’s’s hesitancy about no down payment by emphasizing her security and linking it to the land as collateral and her retention of payments.

Even if the seller needs a down payment, you’ve positioned yourself really well in the initial negotiation by reminding the seller you’ve already agreed to the two terms they wanted (their price and their monthly payment) and have only asked for flexibility on the down payment in return.

Having engaged the seller in an initial conversation and gained insight into their financial needs and concerns, this guide will walk you through the key elements of presenting a compelling $0 down offer that highlights the benefits for them.

Your Objective: To frame the $0 down scenario not as a personal request, but as a strategic solution that addresses the seller’s potential worries and aligns with their motivations.

Use these strategies to pitch terms as a solution, not a risk:

1. “Start Cash Flow Day 1 – No Waiting for a Down Payment”

Problem: Sellers worry about gaps in income if the property sits unsold.

Solution:

“With $0 down, your monthly payments begin immediately at closing. No waiting months (or years) for a buyer to save up a down payment. You replace uncertainty with instant, predictable income.”

2. “Higher Interest Rates Offset the $0 Down”

Problem: Sellers fear losing money without a down payment.

Solution:

“We’ll structure the loan with a higher interest rate (e.g., 8% instead of 6%). This means you’ll earn more total interest over the life of the loan, compensating for the lack of a down payment.”

3. “Shorter Loan Terms = Faster Full Payout”

Problem: Sellers want income now but also want to recoup the full sale price sooner.

Solution:

“By shortening the loan term (e.g., 5 years instead of 10), you’ll receive larger monthly payments and own the asset free-and-clear faster. This reduces long-term risk while keeping income steady.”

4. “Balloon Payments Secure Your Future Windfall”

Problem: Sellers worry about inflation or future financial needs.

Solution:

“Add a balloon payment clause requiring the buyer to refinance or pay the remaining balance in 3–5 years. This guarantees you a lump sum later to fund retirement, reinvest, or cover emergencies.”

5. “Legal Safeguards Protect Your Income”

Problem: Sellers fear buyer defaults.

Solution:

“The property stays collateral. If the buyer misses payments, you retain ownership and keep all payments received—so you’re never left with zero income or an unsold property.”

6. “$0 Down Makes The Monthly Payment Sustainable”

Problem: Sellers assume offering $0 down attracts risky buyers who are likely to default.

Solution:

“I know where you’re coming from, however in my case I offer good credit. I love the property and have never missed a payment in my life. The $0 down payment makes all the monthly payments affordable, which means you can count on predictable monthly payments through the life of the loan.”*

By following this guide, you can structure your $0 down pitch in a way that directly addresses the seller’s potential concerns and highlights the compelling benefits they can gain from owner financing, even without a traditional down payment.

")

How to Buy Land and Subdivide It for Profit Table of Contents Introduction Land Scams